An Explanation of Benefits (EOB) is a statement from your health insurance company that outlines how a claim was processed. It’s not a request for payment — though many people mistake it for a bill. Instead, it’s a detailed summary of the services you received, what your provider charged, what your insurance covered, and what portion (if any) you may owe. Think of it as a receipt that shows the behind‑the‑scenes math of your healthcare costs.

What makes EOBs so valuable is the transparency they provide. They show whether your provider billed correctly, whether your insurance applied your benefits accurately, and whether you’re being asked to pay the right amount. In a healthcare system where costs can feel unpredictable, the EOB is one of the few documents designed to give you clarity rather than confusion.

Why EOBs Matter More Than You Think

It’s easy to overlook an EOB, especially when you’re juggling appointments, prescriptions, and follow‑up care. But reviewing it carefully can protect you from unnecessary expenses. Billing errors are more common than most people realize — duplicate charges, incorrect procedure codes, or services you never received can slip through the cracks. Your EOB is your first line of defense against these mistakes. Beyond error‑checking, EOBs help you understand how your insurance benefits are being used. They show how much of your deductible has been met, how close you are to your out‑of‑pocket maximum, and how cost‑sharing (like copays and coinsurance) is applied. This information can help you plan future care, anticipate costs, and avoid surprises. In other words, your EOB isn’t just paperwork — it’s a financial roadmap.

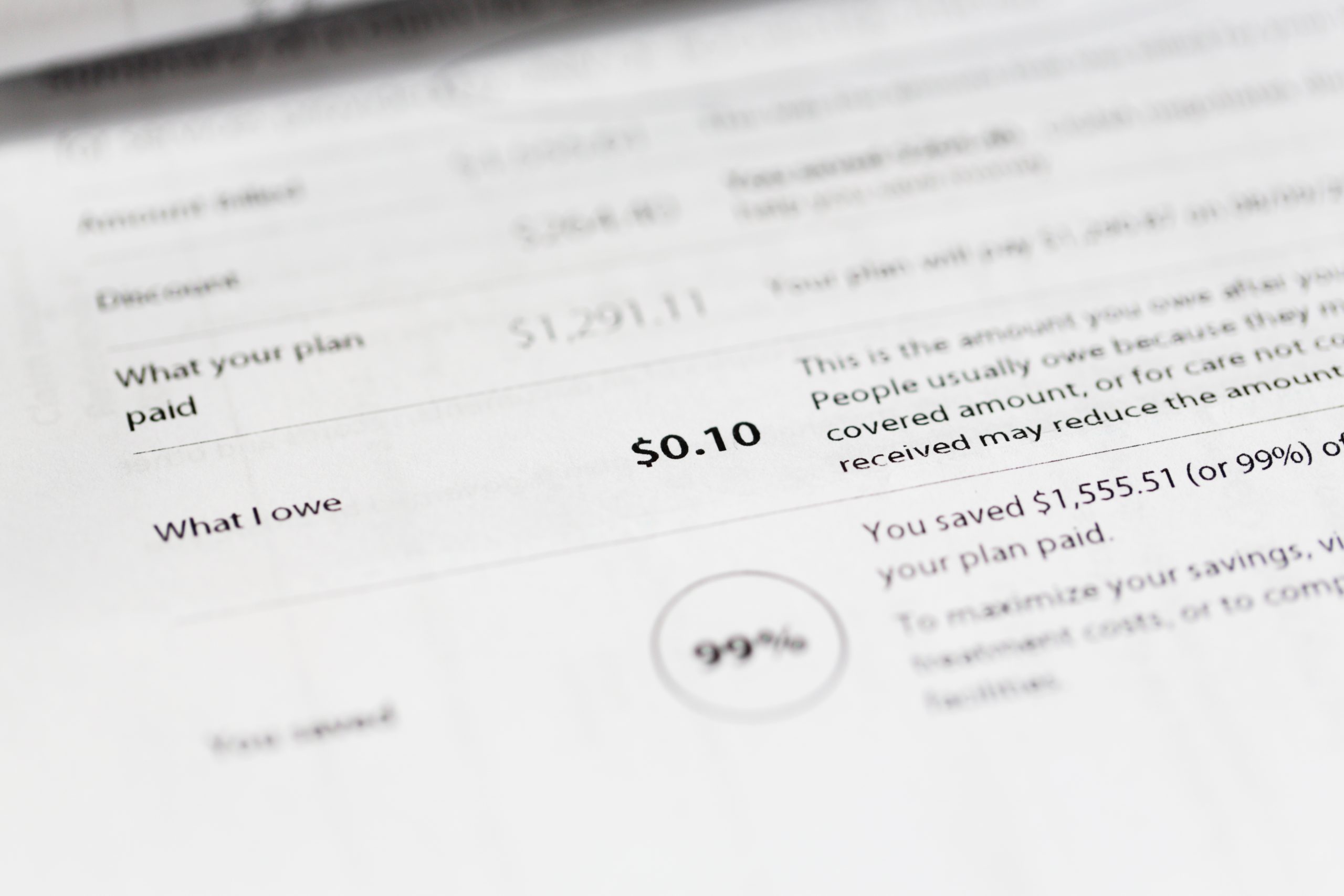

How to Read Your EOB

The layout of an EOB varies by insurer, but most include the same core elements. You’ll typically see the date of service, the provider’s name, the services performed, the amount billed, the amount allowed by your insurance, the portion paid by the insurer, and the amount you may owe. Once you understand these sections, the document becomes far less intimidating. A helpful next step is to compare your EOB with any bill you receive from your provider. The numbers should align. If they don’t, it’s a signal to call your provider or insurer for clarification. Many discrepancies are simple errors that can be corrected quickly when caught early. And if something doesn’t make sense, don’t hesitate to ask questions — your insurer’s customer service team is there to help you interpret the details. The more familiar you become with your EOBs, the easier it becomes to spot patterns, understand your coverage, and make informed decisions about your care.