Not all dental plans are made equal, and not all dental plans cover orthodontics. If you or one of your children are looking to start braces, it’s best to double-check your policy before going forward. The average cost of orthodontic care can vary between $5,350 – $12,000, which are steep costs to be paying out of pocket. Most dental insurance policies separate dental care into three categories:

- Preventive care: Refers to cleanings, oral exams, and X-rays, and other services you may get in a routine dentist’s appointment. Most dental plans cover the costs for these services.

- Basic procedures: These procedures are slightly more complex than routine care and include things like extractions, filings, and gum disease treatment. Basic procedures may be partially covered by dental insurance, with the rest paid out of pocket.

- Major procedures: Refers to more in-depth procedures like crowns, bridges, dentures, root canals, or inlays. Dental insurance may partially cover major procedures, but often at a smaller percentage than basic procedures.

Orthodontics is a separate category from the three mentioned above and is often not included in standard dental policies. If orthodontics is included, the policy may only apply to dependent children.

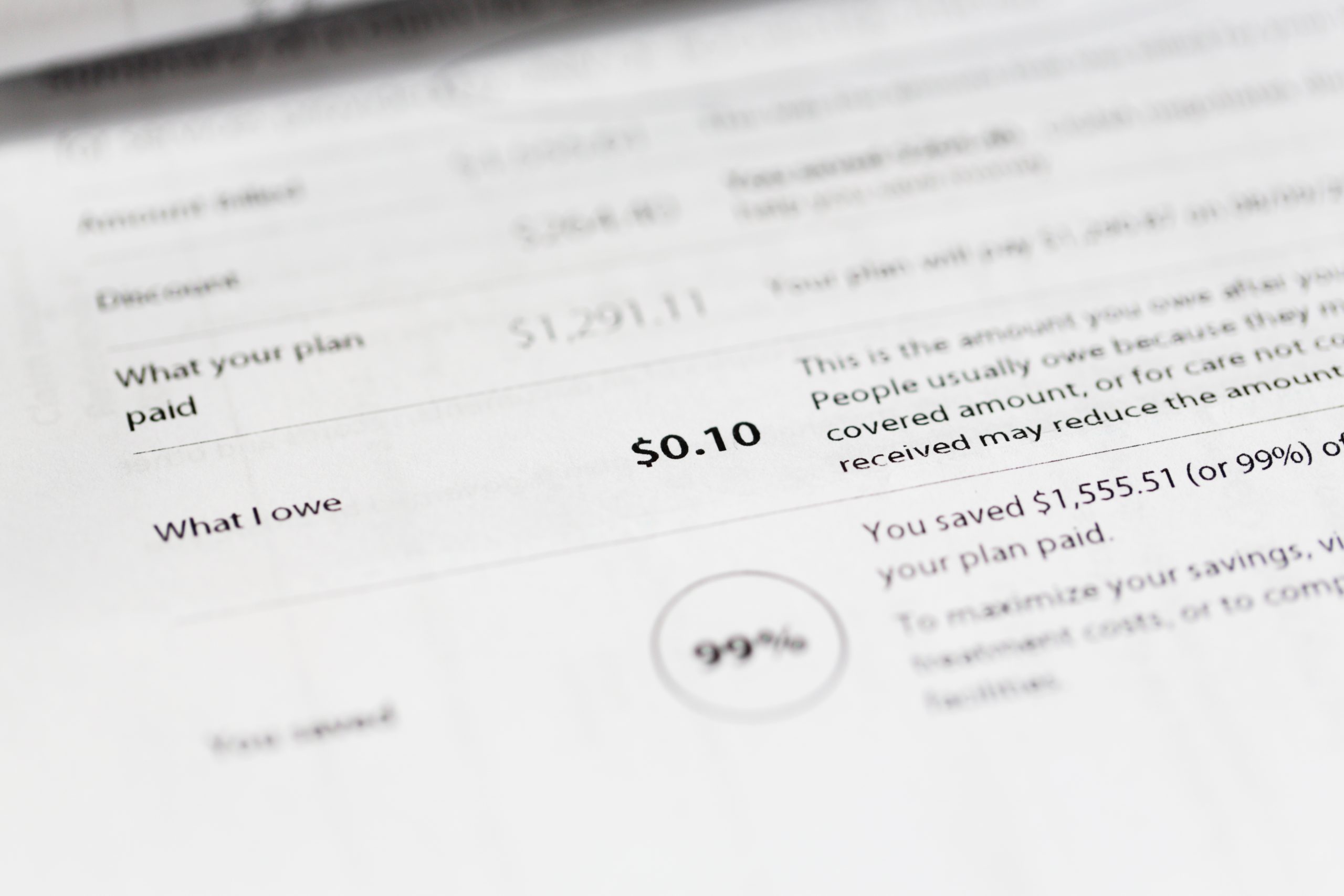

If your dental plan covers orthodontics, you’ll want to be aware of coinsurance amounts and annual and lifetime maximum benefits. For example, a dental plan that covers 50% with a lifetime maximum of $1,000 will only cover $500 of the cost of braces — 50% of the $1,000 lifetime maximum. Every dollar spent after that will need to be paid out of pocket.

Cigna offers orthodontic coverage on select plans. Their full-coverage dental insurance plans often include orthodontics, and, on the plans that don’t cover orthodontics, may include discounts for those procedures. Some Cigna plans have waiting periods, which means you can’t start using the plan’s benefits immediately. For basic procedures, you may need to wait 6 months before the coverage applies, while major and orthodontic services may require you to own the policy for at least a year.

Guardian offers orthodontics on several different plans. Each of their plans have a waiting period of 1 year before the coverage applies. It’s also important to note that Guardian’s orthodontic coverage only applies to children under the age of 19.

Anthem plans may be slightly higher than Cigna and Guardian, but their waiting period is much shorter. Waiting periods on Anthem’s more in-depth plans can vary from none at all to 6 months. Orthodontics are only covered on select plans, so be sure to double check with your provider that your procedures will be covered.

If you qualify for Medicaid, your child’s braces may be covered if they are deemed medically necessary. The Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) benefit provides preventive healthcare to Medicaid-enrolled children under the age of 21 if a screening reveals a condition that needs treatment. This includes orthodontics.

If you’re already on a dental plan, supplemental orthodontic insurance may be an option. This allows you to add coverage for braces and other related services to an existing dental plan. Not all insurance companies offer supplemental insurance, so check with your provider to see if this is an option for you.

It’s important to understand what is and isn’t covered under your dental plan, especially when it comes to orthodontic investments. Always double-check your benefits, coverage amounts, and annual and lifetime maximums to ensure you’re getting the most out of your plan (and paying the least out of pocket).

Braces for adults are often considered cosmetic procedures, so insurance may not cover the cost.